50-Year Mortgages: Cheap Money, Big Opportunities for Savvy Investors

Dustin Overton, REALTOR with Blue Marlin Real Estate - Brevard County FLORIDA • November 24, 2025

What Is a 50-Year Mortgage, Really?

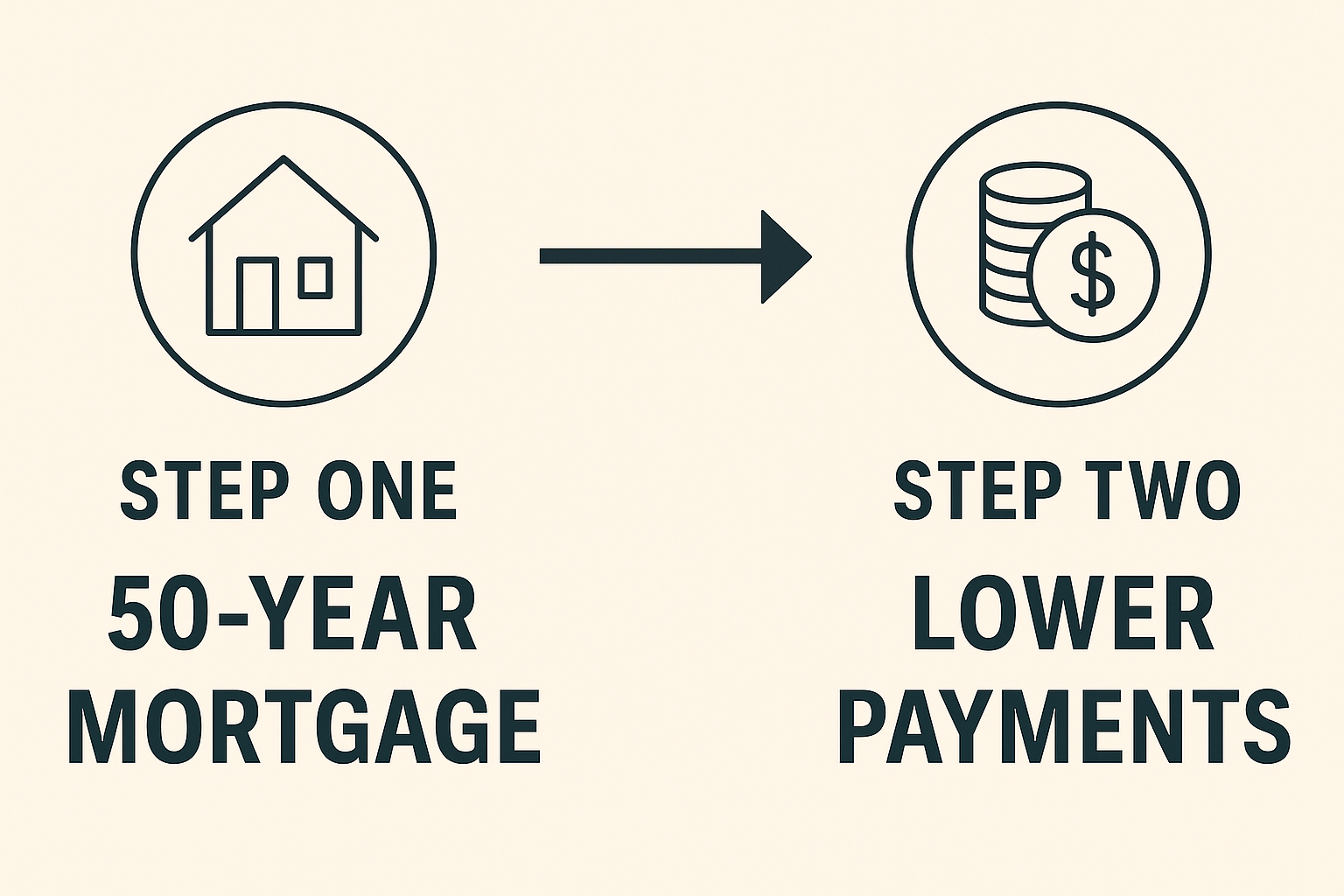

A 50-year mortgage is just a home loan stretched over 50 years instead of the typical 15 or 30.

- Much lower monthly payment than the same price on a 30-year

- In exchange, you pay more interest over time

- Often available only through specialty or non-traditional lenders

It’s not free money.

It’s

cheap monthly money—and that’s where the opportunity lives.

Why Investors Are Paying Attention

For investors, the goal is simple: control good assets with as little monthly out-of-pocket as possible while rents and values grow. A 50-year mortgage can help with that.

Key perks for investors:

- Better cash flow: Lower principal + interest payments can widen the gap between rent collected and total expenses, giving more cushion for vacancies, repairs, and surprises.

- Easier to scale: Lower payments ease debt ratios, making it easier to qualify for more properties and carry multiple doors without getting crushed by overhead. Many investors see 50-year loans as a bridge structure—“I won’t keep this for 50 years, I’m just using it to acquire more doors.”

- Leaning into inflation: If rents and values rise while your payment stays mostly fixed, inflation slowly eats away at the real cost of that debt. You’re using tomorrow’s more expensive dollars to pay back today’s cheaper money.

Benefits for “Regular” Buyers

You don’t have to be a big investor to benefit. For first-time buyers or people coming into higher-price areas, a 50-year term can:

- Make the difference between renting vs. owning

- Let you buy now, then refinance if rates or your income improve

- Free up monthly room to pay off higher-interest debt, save, or invest elsewhere

Think of it as a tool to create breathing room, not a forever marriage.

The Trade-Offs (Still Real)

The flipside:

- More interest over time: Total interest paid is higher than a 30-year. That’s the cost of stretching the timeline.

- Slower equity: Early payments are mostly interest, which can leave you more exposed if the market dips.

- Non-standard terms: 50-year products can have higher rates, stricter underwriting, or prepayment penalties.

Before signing, ask your lender:

- Is the rate fixed or adjustable?

- Any prepayment penalties?

- What happens if I refinance in 3–5 years?

- What’s my total interest vs. a 30-year?

How to Use a 50-Year Mortgage Wisely

Used strategically, a 50-year mortgage is just one piece of a bigger plan:

- Acquire: Use it to buy in a market you believe in while the numbers still work.

- Stabilize: Enjoy the improved cash flow and let rents catch up.

- Upgrade: When rates, equity, or income improve, refinance into a shorter term or start making extra principal payments.

Cheap monthly money can be a ladder if you climb it on purpose.

For any inquiries about real estate in Brevard County Florida - Please contact Dustin Overton with

Blue Marlin Real Estate - The #1 Brokerage on the Space Coast

River Fly-In 735 Pilot Lane Merritt Island, a waterfront aviation-focused condo community with Sykes Creek views, resort amenities, garage parking, and EV charging.

Move-in ready Rockledge home with new roof, fresh interior, tropical fenced yard and no HOA—perfect for first-time buyers or downsizers.